What Happens When Capital Has Nowhere Left to Go?

The overlap between legal and criminal activities arises from a lack of appropriate regulation and enforcement. These conditions have led to the legal and illegal trade in wild species being functionally inseparable. Right now, no matter what companies, governments, NGOs and academics try to promote, the reality is for all but literally a handful of species, that it is difficult to genuinely prove if they were legally harvested.

The lack of regulatory proof begs the question, is this trade best described as pseudo-legal, defined, say, as legalised by neglect? This is how illegally harvested species (and their financial value) flow into the global supply chains, through the pseudo-legal (legal by neglect) marketplace. Transnational crime associated with trade, including the trade in wild species, cannot be genuinely tackled without a system that also addresses white collar, corporate crime. This system has never really existed. While companies worldwide admit there is likely to be green crime in their supply chains, they can make these statements with impunity because little is ever done.

What too few want to acknowledge is that there is no point focussing on ‘wildlife crime’ without bringing the pseudo-legal – legalised by neglect – activity into the picture.

This approach is by no means unique to the trade in wild species. The same problems have emerged with investments, made easier because business, investors and governments in Western economies have, since the 1980s, shifted to ‘capital-light’ sectors.

Outsourcing to low-wage countries shifted Western economies away from heavy capital (productive) investments, like manufacturing, toward services, requiring less physical capital per unit of output. In parallel, companies have been incentivised to boost share prices, including through share buy-backs.

The profitability and viability of this shift is reliant on ever-growing consumption, and this is no longer happening. Consumption is increasingly reliant on the rich, as normal people have seen a continuous decline in disposable incomes. The wealthiest 10% are now responsible for 50% of consumption in the US. This means there is no scope for high returns from productive investments without massive redistribution, which is not seen as politically possible as yet. Productive investments and even capital-light investments in services are no longer paying off in the West.

At present, financial investments are still paying off, but there is growing evidence that we are on the brink of another financial crisis caused by excessive private debt and misallocation of capital, due to the lack of opportunities in productive investment and light-touch regulation.

So, what happens when productive investments aren’t paying off, regulation has been severely hollowed out, and financial investment opportunities are looking increasingly risky?

Investors are still chasing returns, and the only place to go to chase returns outside the stock market leaves semi-criminal / fraudulent / scam / gambling opportunities. This has been made increasingly easy thanks to the lack of transparency and lack of curiosity to look beyond the PR spin masquerading as analysis put out by businesses and managed funds alike. As a result, investors are just as much in the dark as everyone else.

Investigative journalism in the MSM is all but dead, with the MSM now complicit participants in maintaining the illusion of a functioning capitalist system.

The current situation has also been created in part by a number of measure that governments put in place to deal with the fallout from the GFC.

Firstly, in the decade following the 2008 GFC capital was effectively free, due to the Zero Interest Rate Policy (ZIRP) used by a country’s central bank to set its benchmark interest rate at or very near 0%. Because capital was effectively free, this led to an era of ‘growth-at-all-costs’ which has led to a massive cash burn and bubble in private debt.

Most of the effectively free capital has flown into asset price inflation (stock market, residential property) and into private equity investment. The latter is not regulated or transparent and likely sitting on massive piles of unpayable debts with (worthless) zombie companies as collateral. All these funds can do is sell to each other to obscure the lack of profitable exit opportunities.

Second has been the gutting of regulators and regulations. Lack of regulation or capture/gutting of the regulator is resulting in a lack of enforcement which in turn enables non-penalised criminal activity in existing markets.

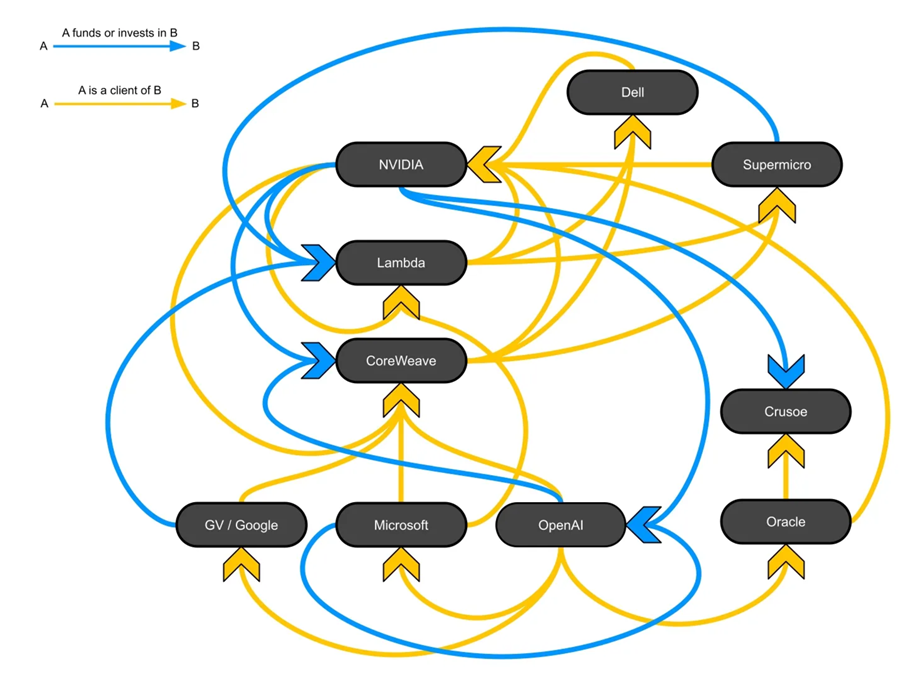

Junk fees and circular investment are examples of this, with the latter being perfectly demonstrated by the AI economy, well described here:

Third has been the creation of new ‘asset’ classes that are essentially gambling tokens (cryptocurrency, NFT) in a mostly unregulated environment. This has enabled large-scale fraud, scams and also created a non-transparent payment system for real criminal activity (drugs, arms, people, wildlife).

As long as new money can be created easily (90% of new money is created by commercial banks through issuing new loans) and interest rates remain low, the move into questionable and criminal activity will continue.

Investment needs returns and non-prosecuted fraud produces high payoffs. Fines, on the few occasions they do happen, are not a deterrent but just a cost of business.

What has created this mess, and continues to create an even bigger one, is nicely summarised by Oliver Bullough in a recent article, Why the law lets financial criminals off the hook. In the article Bullough writes, A couple of years ago, an adviser to a senior politician here in the UK asked me for some suggestions for policy proposals for tackling financial crime. I told him I’d like more resources for law enforcement agencies. His reply: “that’s not going to get us many headlines, is it?”

He goes on to say, “This story is intended to illustrate how one of the reasons for the world’s failure to stop money laundering is that politicians are addicted to the sugar rush of new policy announcements, but shun the hard work of enforcing old ones. But it’s indicative of a problem with journalism too. Journalists like to talk about shiny new things — crypto! AI! — and ignore the old ones that we’ve already reported on.”

The lesson Bullough says is, “rich, powerful men dividing up the world between themselves. Crooks and thieves may invent new tools, but they’re always designed to do the same old job: steal. A world-weary shrug — How is that a story? Bring me something new — just lets them off the hook”

The depth of this crisis was again brought home by Bullough, as he traced Britain’s vital role in the growth of offshore money laundering in his BBC Audio Series How to Steal a Trillion, the Trillion Dollar Laundromat.

In an interview for this BBC series, David Lewis, head of anti-money laundering policy at the UK Treasury between 2009 and 2015 says,

“In the whole of that time I was asked only once what could be done to tackle money laundering, but I was repeatedly asked to justify our money laundering regulations and why we need to comply to global standards and what we can do to reduce the burden of those regulations. I was put in star chambers with ministers where I was grilled about why we have these regulations. They were things like the Red Tape Challenge, policy challenges across Whitehall to get rid of regulations. That meant I spent all of my time trying to defend any action at all on money laundering, let alone taking more action”.

When questionable, semi-legal and illegal financial behaviour goes unchallenged, the response is to push the boundaries more.

So we shouldn’t be surprised that rules created to protect investors, economies, societies and environments continue to be undermined. Right now, even the stock market integrity is being undermined rapidly.

As outlined in Fortune, “To get into the S&P 500, a company is supposed to make some money. The sum of its four quarters of earnings has to be positive—at least GAAP wise—and so does its most recent quarter. That’s a pretty basic rule, decades old and it’s the reason Tesla sat outside of the index until the end of 2020, years after it had become one of the most valuable companies on earth. Soon, that rule will be broken, likely three times. On purpose. SpaceX, OpenAI and Anthropic are all independently preparing to go public. None of those companies yet make money; in fact, SpaceX lost billions last year, and OpenAI and Anthropic are also not profitable. Yet, when they go public, they will be ranked among the largest companies in America; and quickly begin dominating 401Ks and index funds”

SpaceX is expected to have a hefty weighting in the S&P 500 due to its sheer size, which means most people with investment accounts or pension pots will be exposed to its stock market performance as investors in the company. Violating the old rules is about capturing index fund investment and access to trillions of dollars of institutional retirement funds.

Let’s be clear, Space X’s listing represents a huge money-making opportunity for bankers. So it comes as no surprise that Goldman Sachs, Morgan Stanley, JP Morgan, Bank of America and Citigroup are among the 23 banks working on the listing.

Once the old rules have been broken, the old investor protections will be gone. This will enable more fraud and deception and where SpaceX, OpenAI and Anthropic are going, others will follow.

On top of erasing listing rules, work is also underway to ‘tokenize’ the stock market, digitising real-world equities into blockchain-based tokens. This undermines shareholder protection by replacing direct equity ownership with legal ambiguity. The digitisation of real-world equities can erode standard shareholder protections in several key ways, most notably loss of direct ownership and voting rights.

Traditional stock ownership grants legal equity, entitling the investor to proxy voting on corporate governance and executive compensation. Many tokenized assets are derivative wrappers or custodial claims managed by special-purpose vehicles. In these systems, retail token holders do not legally own the underlying stock. The third-party issuer might technically hold the stock and cast proxy votes, stripping the actual investor of their right to influence company policy.

All of this begs the question about the timing of the Wall Street’s top regulator, the Securities and Exchange Commission proposal to end a 55-year-old requirement that U.S. public companies share detailed financial results four times a year, to twice-annual earnings reports, pursuing an idea President Trump has personally pushed.

While most companies stopped providing meaningful financial information long ago, from inventing their own reporting and profit metrics (Uber probably being the most reported example) to no longer reporting basics like revenue and costs from individual business units, the twice annual twice-annual earnings reports is a further shake-up of US corporate governance.

All this means that there is no point focussing on criminal activity without bringing pseudo-legal – legalised by neglect activity – into the picture.

When considering the trade in wild species, all the regulatory deficiencies have been known for so long that they are predictable, and foreseeable, to the point where they have become accepted features of the wildlife trade system. And now the ‘follow-the-money’ type financial investigations to curb wildlife trafficking are equally clinically sidestepping the fact that the lack of financial regulation and enforcement has allowed productive, financial and criminal investments to merge.

The fact that this erosion of standards and regulation is being ignored is a disaster for the environment and society. The rich are rigging the game purely for their own benefit and with disastrous consequences for the rest of us.

While it is a disaster, it is predicable. Peter Turchin’s research into cyclical historical collapses is outlined in his book, End Times: Elites, Counter-Elites, and the Path of Political Disintegration.

In the book Turchin shows how end-of-cycle behaviour typically evolves into a destructive loop where, when elites are provides with a number of options, they always make the most catastrophic decisions for the long-term survival of society. This, he says, happens for a few key reasons:

- Short-term Maximization: Elites prioritise immediate self-preservation and asset protection over the long-term health of the state.

- Zero-Sum Mentality: Rather than expanding the economic pie or sharing power to ease tensions, they restrict upward mobility to preserve advantages for their own descendants.

- Extremism: Intense intra-elite competition breeds ideological extremism. Factions become unwilling to compromise, eventually dismantling institutions to consolidate power and purge their rivals.

Sounds familiar?

The difference this time around is that we live in a global world and this collapse will not be localised as has happened historically.

It seems collectively unhinged to allow a handful of unhinged individuals – what Bullough calls, “rich, powerful men dividing up the world between themselves” – to drag us all down.

But history shows this is the most likely scenario. Welcome to the end times!

The question is, when are we going to start to push back? When will the blatant anger of populations in the West move from rants on X or Facebook and useless ‘protest votes’ into actions that cannot be ignored?

From history, shutting down the economy – by withdrawing labour – is often seen as the only leverage people have over those in power. So, all this comes at an interesting point in time with the International Court of Justice just resolving a 14-year dispute over workers’ right to strike – giving trade unions worldwide a significant win.

From quietly quitting to peaceful protests, is it time for more of us to push back on the growing growing number of predatory systems?

Lynn Johnson is a physicist by education and has worked as an executive coach and a strategy consultant for over 20 years. In her work she pushes for systemic change, not piecemeal solutions, this includes campaigning for modernising the legal trade in endangered species, to help tackle the illegal wildlife trade.